Supply is expected to be tight in Q1, with consumption facing uncertainty. Tighter supply in exporting countries will likely limit global pork trade. On the demand side, rising inflation and high stock accumulated in 2022 will pressure import needs.

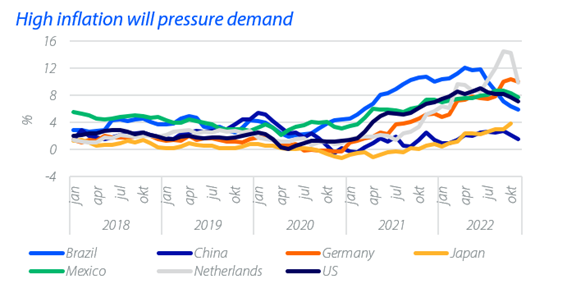

Slowing economy weighs on demand, raising uncertainties and volatility – In a slowing economy, while pork is believed to be less impacted than more expensive proteins, there will still be some pressure on consumption. Pressure on household incomes, increased savings, and a potential decline in specific channels can all pressure consumption. Managing inflation will remain important for many governments, with interest rates needing careful calibration against consumer and business confidence.

Limited upside for trade in 2023, as supply tightens in exporting countries and rises in importing countries – Trade will likely increase modestly in Q1 2023, mainly due to a low base last year. However, it may find growth difficult to sustain through 2023, given the slow production in major exporting regions, mainly the EU and US. By contrast, Brazil, which continued to grow exports in 2022, is expected to increase production and exports this year. The further recovery/growth in local production in Southeast Asia and China will mean demand for imports eases, particularly in 2H 2023.

China re-opening raises opportunities but also uncertainties – As China is the global largest pork market, its reopening will impact the global supply/demand balance. But when, and by how much China’s demand will rebound is uncertain. We expect demand to evolve unevenly, due to ongoing Covid waves, macroeconomic headwinds, and weak business confidence.

Download the full report

These are the main highlights:

North America: The US herd is at an inflection point as the US herd returns to growth, but growth slows in Mexico and Canada. Exports are stronger from the US and Canada as pork is competitive in key markets.

Europe: Pork production is set to tighten further in 2023, with few exceptions. Pig carcass prices remains supported by tight supply and high input costs.

China: Pork prices plunge on short-term volatility, oversupply and weak demand on high Covid infection numbers. Demand expected to rebound late Q1.

Brazil: Easing feed prices should improve margins but Brazil needs stronger Chinese demand to balance supply growth

Southeast Asia: Southeast Asia will see strong production growth despite ASF impacts and high input costs in 2022. Continuous growth expected in 2023.

Japan: Pork consumption manages to remain flat and storage capacity will not allow import to increase.

{kind=link}