Key points:

- Brazilian pork production growth slows to 1% year on year in 2024 and 2025

- Domestic pork consumption eases following firm pricing but forecast to recover in 2025

- Record high exports in 2024 so far look set to continue into 2025

Production

Brazil is the world’s fourth largest pork producer standing behind China, the European Union and the United States. Pork production in Brazil has seen strong grown in recent years following significant industry investment in response to increasing demand on the domestic and global markets. The USDA has revised down its 2024 forecast to year-on-year growth of 1%, down from 3% earlier this year. A further increase of 1% is forecast for 2025 to 4.55m tonnes (CWE). Lower feed costs were said to be incentivising production gains earlier this year, however in recent months this has been limited due to unfavourable weather in spring. Rabobank report that heavy rains in April and May reduced the supply of piglets.

Consumption

Pork is the third preferred protein in Brazil after chicken and beef. USDA forecast domestic consumption to decline by 1% in 2024 due to firm pricing, although there is an expectation of demand picking up towards the end of the year for seasonal activities such as BBQ season, Christmas and New Years celebrations. Looking to 2025, consumption in Brazil is expected to recover, increasing by 2% to 3.07m tonnes (CWE) following stronger economic signals in recent months.

Trade

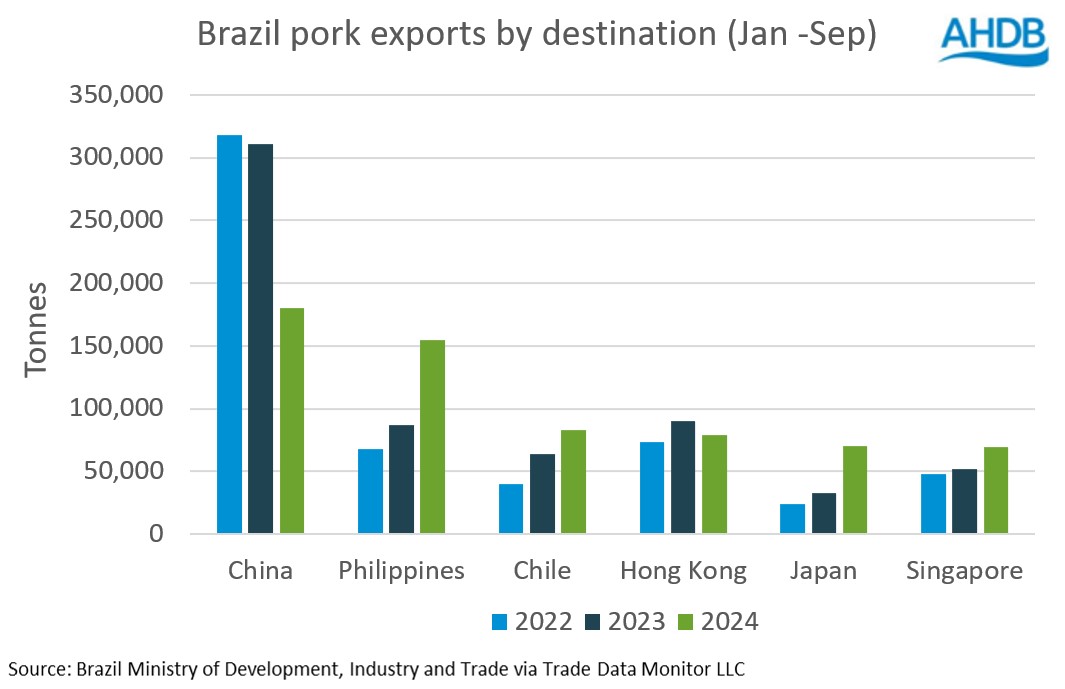

Total pig meat exports (including offal) from Brazil have grown 5% (53,000 tonnes) for the year to date (Jan-Sep) compared to 2023, at 1.05m tonnes. This is the highest volume of pigmeat exported by Brazil on record.

Brazil’s top export destinations are China, the Philippines, Chile, Hong Kong, Japan and Singapore. Volumes to China and Hong Kong have declined year on year but increased to all other major destinations. Although China remains the largest export destination for Brazilian pig meat, volumes fell by 42% (131,000 tonnes) in 2024. The volume decline for Hong Kong was smaller but still significant, down 13% (12,000 tonnes). However, shipments to the Philippines jumped up by 68,000 tonnes (79%). Chile has replaced Hong Kong as the third largest destination with volumes increasing 19,00 tonnes in 2024 so far. Japan has also climbed the rankings, overtaking Singapore with a volume gain of 38,000 tonnes. Singapore recoded the smallest change of all the major trade partners, up 17,100 tonnes.

Current trends are forecast to continue through to the end of the year, with potential to carry on into 2025. Brazil is capitalising on price competitiveness, outcompeting some key European countries on Asian markets. Despite pig meat import demand from China declining, there may be space for Brazil to further increase its market share depending on the outcome of the Chinese antidumping investigation on European product. Markets in the wider Southeast Asian region are likely to remain lucrative with strong demand and limited production capacity due to continued disease outbreaks. Recently Brazil has obtained authorization from Malaysia to export pork and offal.

Global markets are expected to firm up with seasonal demand as we approach Christmas. However, many current geopolitical issues will roll into the new year such as the conflict in the middle east and the new US government may introduce trade policy changes.

{kind=link}