James Mintert and Michael Langemeier, Purdue Center for Commercial Agriculture

A breakdown on the Purdue/CME Group Ag Economy Barometer December results can be viewed at https://purdue.ag/barometervideo. Find the audio podcast discussion for insight on this month’s sentiment at https://purdue.ag/agcast.

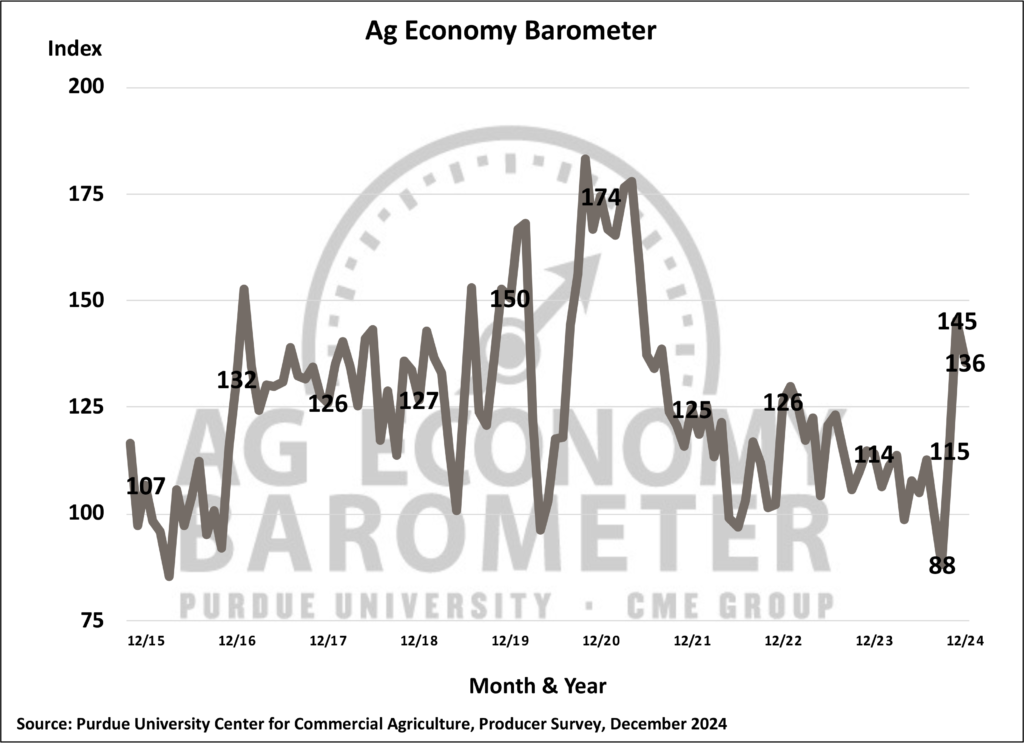

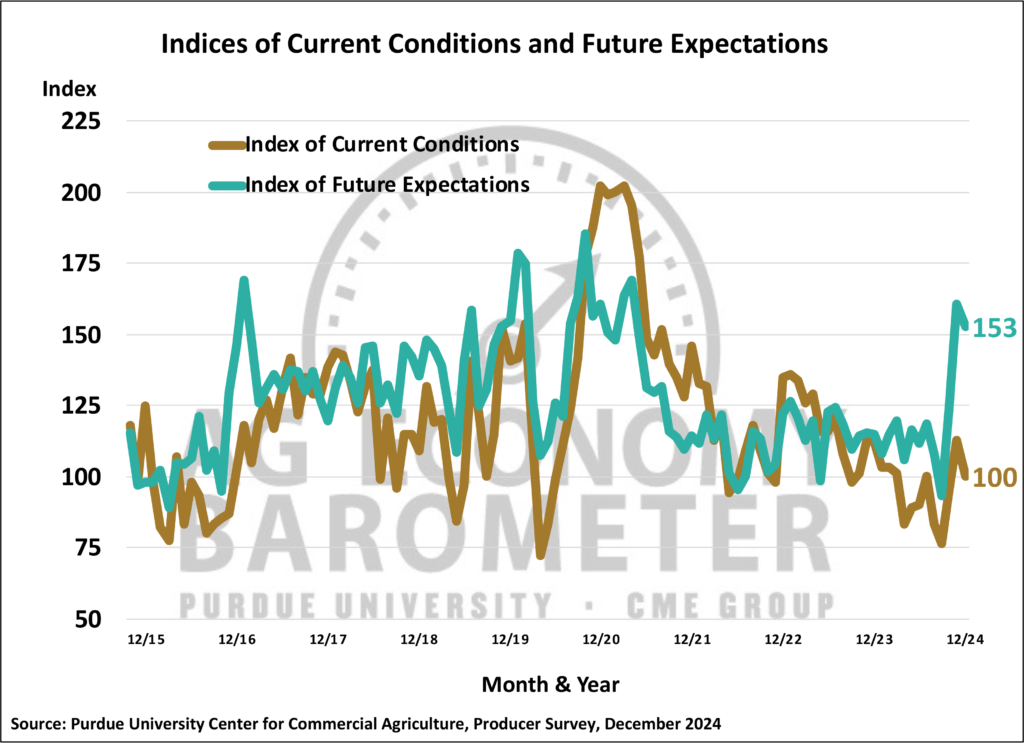

Farmer sentiment drifted lower in December as the Purdue University-CME Group Ag Economy Barometer fell 9 points to 136. Although the barometer weakened somewhat in December compared to November, producers still retained much of their post-election optimism about the future. The Index of Future Expectations dropped just 8 points to 153, leaving that index 59 points higher than in September and 29 points above the October reading. The Index of Current Conditionsdeclined 13 points to 100, indicating that producers’ appraisal of current conditions in U.S. agriculture and on their farms is weaker than their views regarding the future. Despite this month’s decline, the Current Conditions Index remains 24 points above its September low and 5 points higher than in October. Optimism about the future appears to be motivated primarily by producers’ expectations for a more favorable policy environment in the years ahead. The December barometer survey took place from December 2-6, 2024.

Farmers’ views about the current situation and the one-year ahead outlook differed noticeably from their five-year ahead outlook. Overall, responses to questions focused on the current situation and outlook over the next 12 months were weaker than a month earlier, while responses to questions focused on the outlook over the next five years tended to be more positive than in November. For example, the percentage of respondents who expect widespread good times in U.S. agriculture over the next five years rose to 57%, up from 52% a month ago and 34% in October. The expectation for good times extended to both the crop and livestock sectors, with the percentage of respondents expecting good times increasing by 4 points for crops and 5 points for livestock. However, when asked about financial conditions on their farms today compared to a year ago, the percentage of respondents reporting worse conditions today rose to 57% in December compared to 51% in November. When asked for their outlook for the U.S. agricultural economy over the next 12 months, 51% of producers in December said they expect bad times compared to 40% of respondents who felt that way in November.

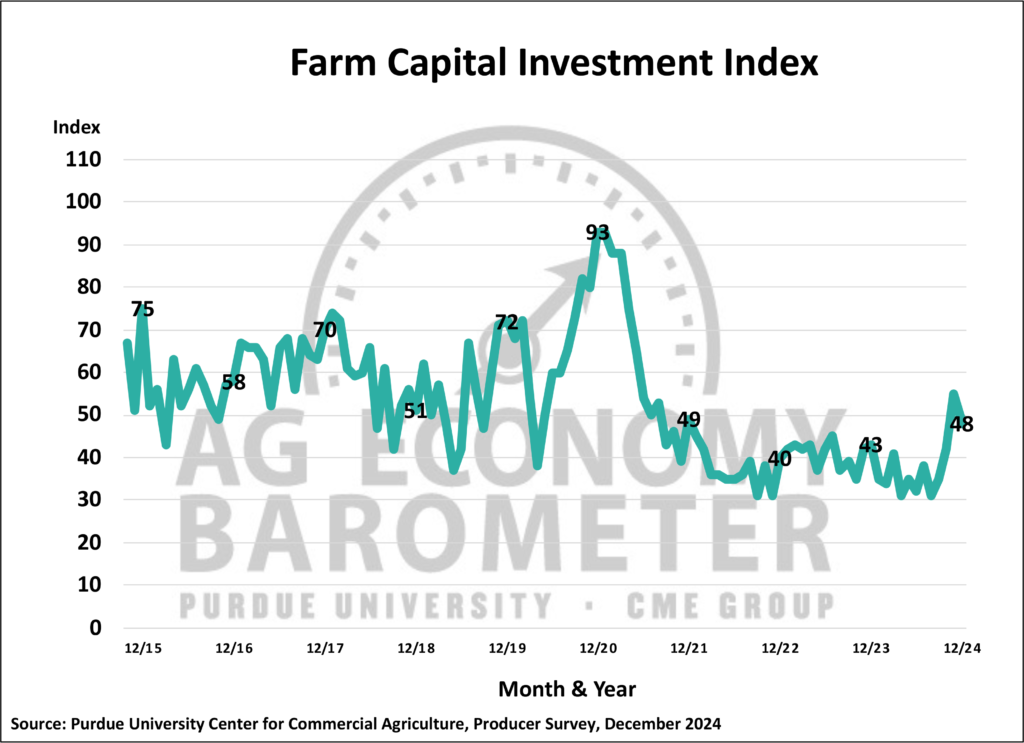

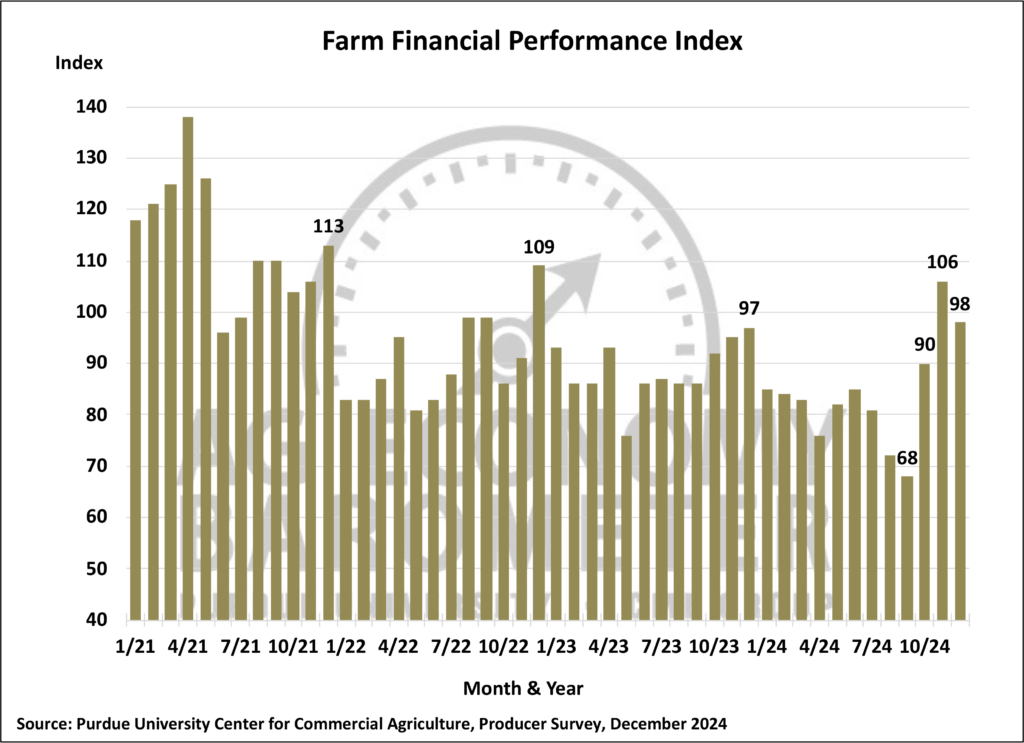

The Farm Capital Investment Index fell 7 points in December to a reading of 48. This month’s decline came on the heels of a 13-point rise in November. The percentage of respondents who said it’s a good time to invest declined to 17% compared to 22% a month earlier, while the percentage of farmers who said it’s a bad time for investments rose slightly to 69%, up from 67%. The investment index’s decline mirrored that of the Farm Financial Performance Index, which fell 8 points in December to 98.

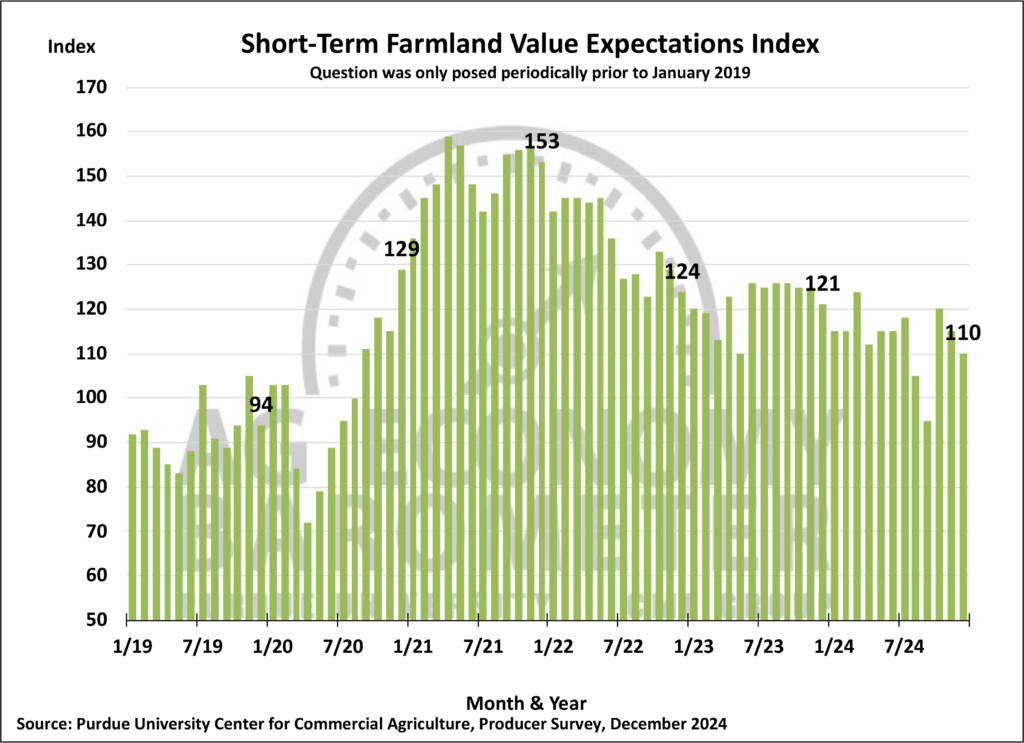

The Short-Term Farmland Value Expectations Index fell 5 points in December. This month’s decline follows a 5-point decline in November. Despite two months of declines, at 110, the short-term index remains 15 points above its late summer reading of 95 in September. The Long-Term Farmland Value Expectations Index, which is derived from a question that asks producers to look ahead 5 years, was down just 1 point from a month earlier, leading to a reading of 155.

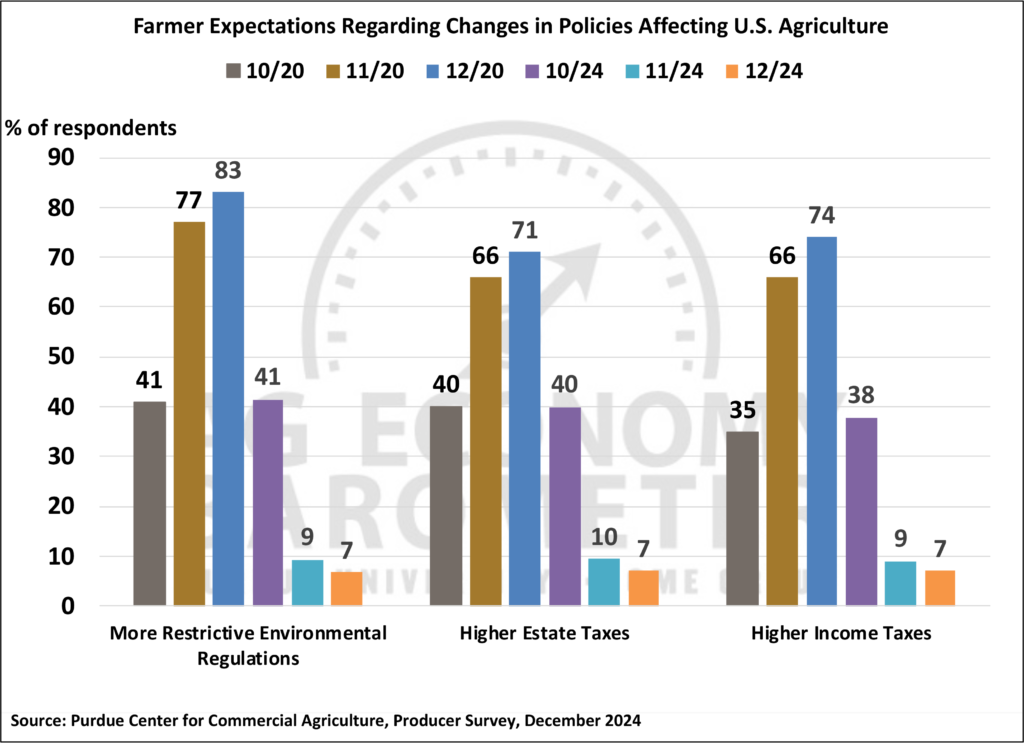

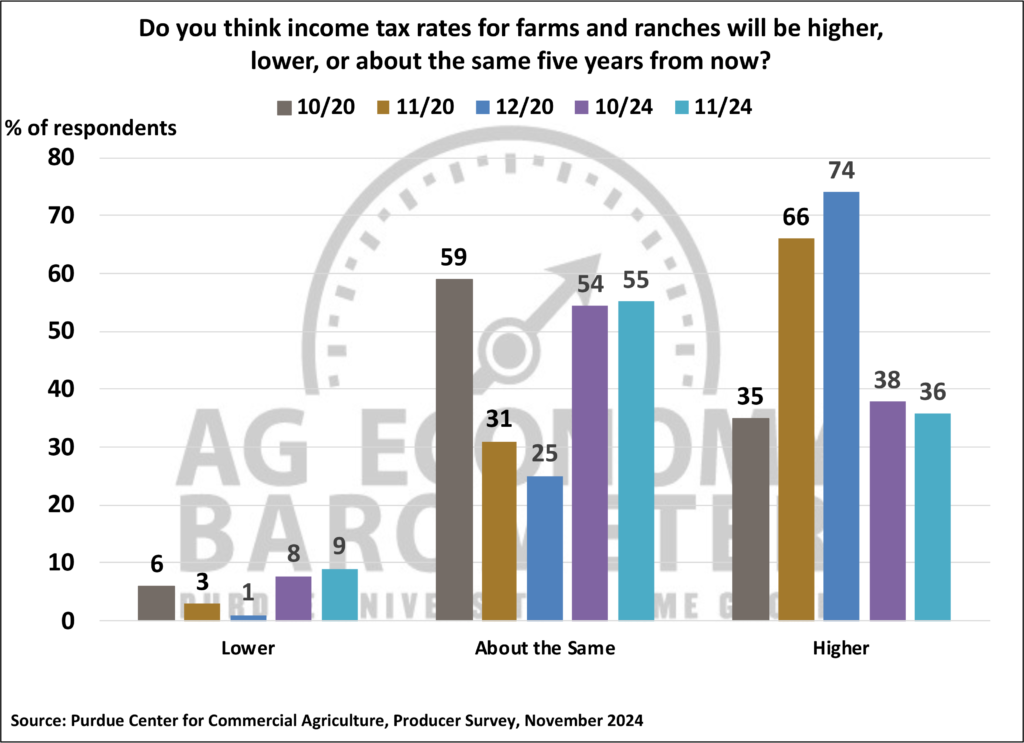

Farmers’ future outlook for their farms and the agricultural sector remains noticeably more positive than at the end of summer. The drivers behind producers’ improved outlook for the future appear to be expectations for policy shifts following the November 2024 election. Expected policy shifts include environmental, estate and income tax policies. Prior to the election, over 40% of producers said they expected to face more restrictive environmental regulations over the next five years. Following the election, less than 10% of producers said they expected a more restrictive regulatory environment. Before the election, 40% of farmers in our survey said they expected estate taxes to rise in the future. After the election, fewer than 10% said they look for estate taxes to rise within the next five years. Additionally, leading up to the election, nearly four out of ten (38%) producers said they expected income taxes to rise in the future. Following the election, that percentage also fell below 10%. Finally, over half (55%) of respondents to the December survey said they expect the fall 2024 election outcome to lead to a stronger farm income safety net than was in place prior to the election.

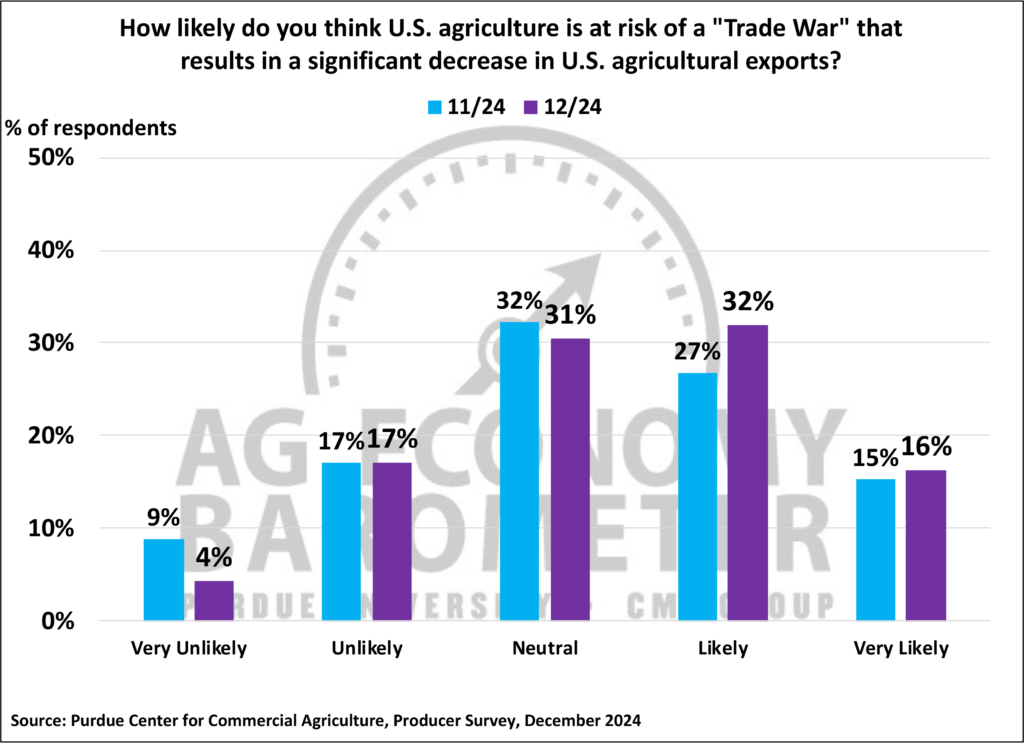

One area of concern for U.S. farmers continues to be the future of international trade in agricultural products. Both the November and December barometer surveys asked producers about the likelihood of a ”trade war” breaking out that has a negative impact on U.S. agricultural exports. Results reveal that many producers are concerned about this possibility. In December, 48% of farmers said they think a “trade war” that negatively impacts agricultural exports is either likely (32%) or very likely (16%). That’s up from 42% of respondents who felt that way in November. On the other end of the spectrum, just 21% of December’s respondents said that a “trade war” was either unlikely (17%) or very unlikely (4%). That’s down from 26% of farmer respondents who felt that way in November. Finally, when asked which policies or program will be most important to their farm in the next five years, “trade policy” emerged as the top choice in December, selected by 43% of producers, with “crop insurance program” trailing as the second-most common response at 17%.

Wrapping Up

Farmer sentiment weakened in December, with concerns about the current situation on their farms and U.S. agriculture as the primary driver behind the sentiment decline. Although expectations for the future also weakened in December compared to November, it was clear that U.S. producers continued to be markedly more optimistic about the future than they were as recently as September. Expectations among farmers for more favorable regulatory, estate tax and income tax policies over the next several years explain much of the optimism about the future. However, the possibility that a “trade war” could break out that has a negative impact on U.S. agricultural exports is a rising concern among farmers, with more farmers expressing concerns about agricultural trade in December than in November.

{kind=link}