Key points

- US pork production is forecast to increase by 3.1% year on year to 12.8 million tonnes in 2024

- Steady to firm demand in the domestic and export market support higher pricing

- US export figures have increased by 6.1% in the year to date (Jan-May)

- Imports of pig meat to the US have grown 7.5% year on year (Jan-May)

Supply

The US inventory of all hogs and pigs stood at 74.5 million head on 1 June 2024, an increase of 1% from June last year. Growth in the number of fattening pigs (up 2% to 68.5 million head), outweighed decline in the breeding herd (down 3% to 6.01 million head).

For the year to date (Jan-May), the US has produced 5.3 million tonnes of pork, 1.9% ahead of the volumes produced during the same period last year. This growth has been driven by productivity gains with slaughterings totalling 53.9 million head for the period, up 2.3% compared to last year. According to the latest USDA data, US pork production is forecast to reach 12.8 million tonnes in 2024, a 3.1% increase on 2023.

Average carcase weights remained higher year on year in May and June further supporting production. The seasonal decline in weight usually seen during summer is not yet showing, with reports suggesting that stronger pig prices and lower grain prices are encouraging some producers to maximise weight gain.

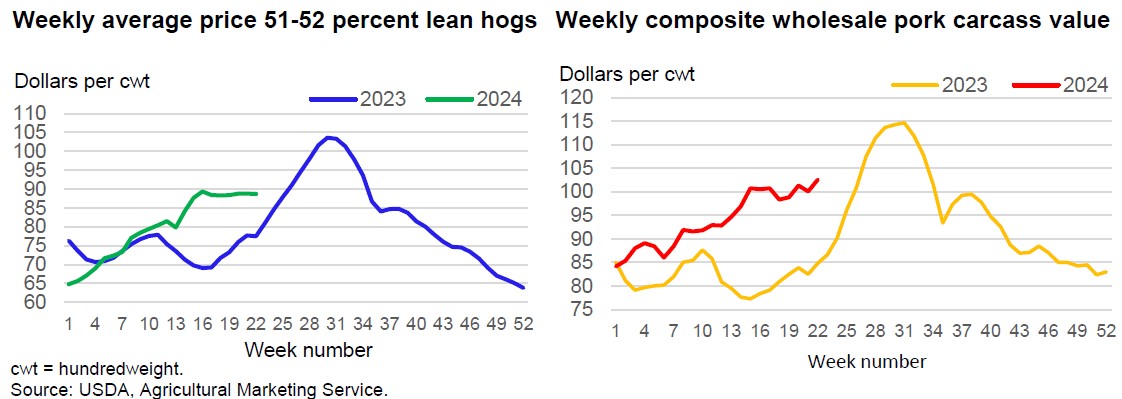

Prices

Since the end of January, US pig prices have been trading above 2023 levels. Average live weight equivalent prices in May recorded an increase of 19.5% year on year but have steadied in recent weeks. The wholesale market has also seen a firm trend upwards in 2024 compared to year ago levels. Higher prices for bellies, loins and ribs have been reported to support the value of the whole carcass through June.

Robust pricing coupled with lower feed costs has resulted in healthy margins for some producers. Iowa State University’s Estimated Returns for Iowa Farrow-to-Finish operations show positive returns in May of $17.06/head. Steady to firm demand in the domestic and export market are expected to keep prices supported in the coming months.

Copyright: USDA, Economic Research Service

Trade

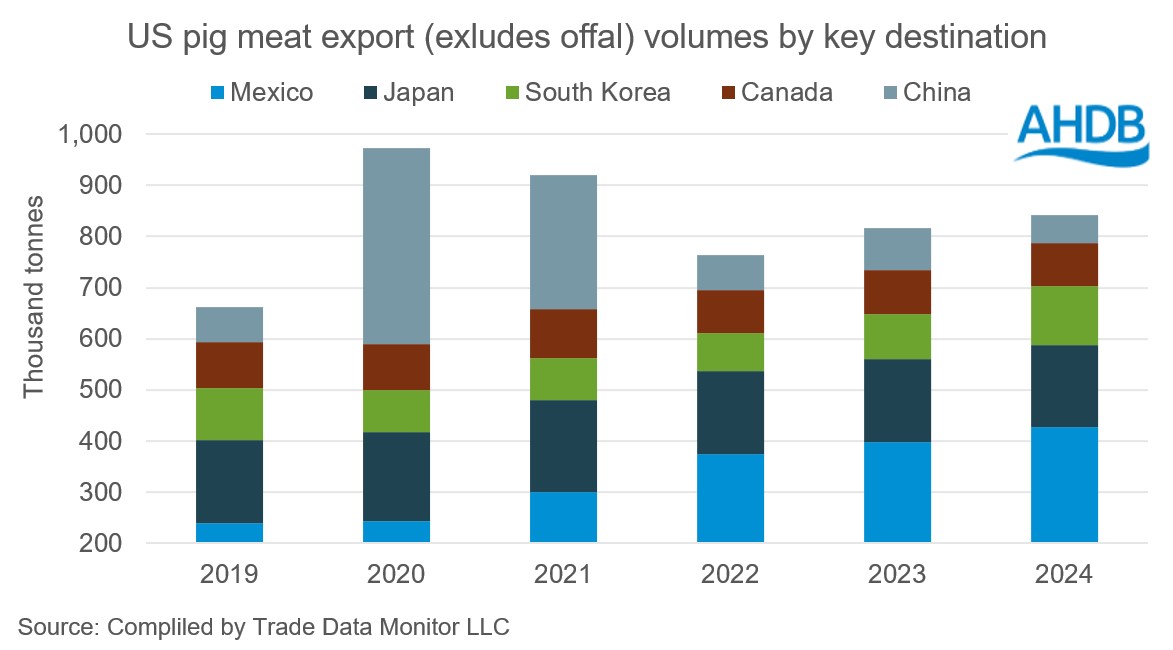

Despite higher pricing year on year, US pork is competitive on the global market due in part to lower feed costs and reduced shipping rates in comparison to the EU27 and UK. For the year to date (Jan-May) US pig meat exports (excluding offal) totalled 1.09 million tonnes, an increase of 6.1% year on year. Good supplies paired with competitive pricing has resulted in significant increases in volumes shipped to most of the key destinations with the exception of China, Dominican Republic and Canada.

Mexico is the dominant destination for US pork exports, with a 40% market share of volume. Volumes shipped to Mexico have continued to strengthen year on year up 29,100 tonnes so far in 2024. Meanwhile, shipments to South Korea, Australia and Columbia have also seen significant growth, up 27,000 tonnes, 15,300 tonnes and 14,600 tonnes respectively.

Rabobank are forecasting US pork exports to end the year at 6% growth, with improved demand anticipated from Asia in the second half of the year.

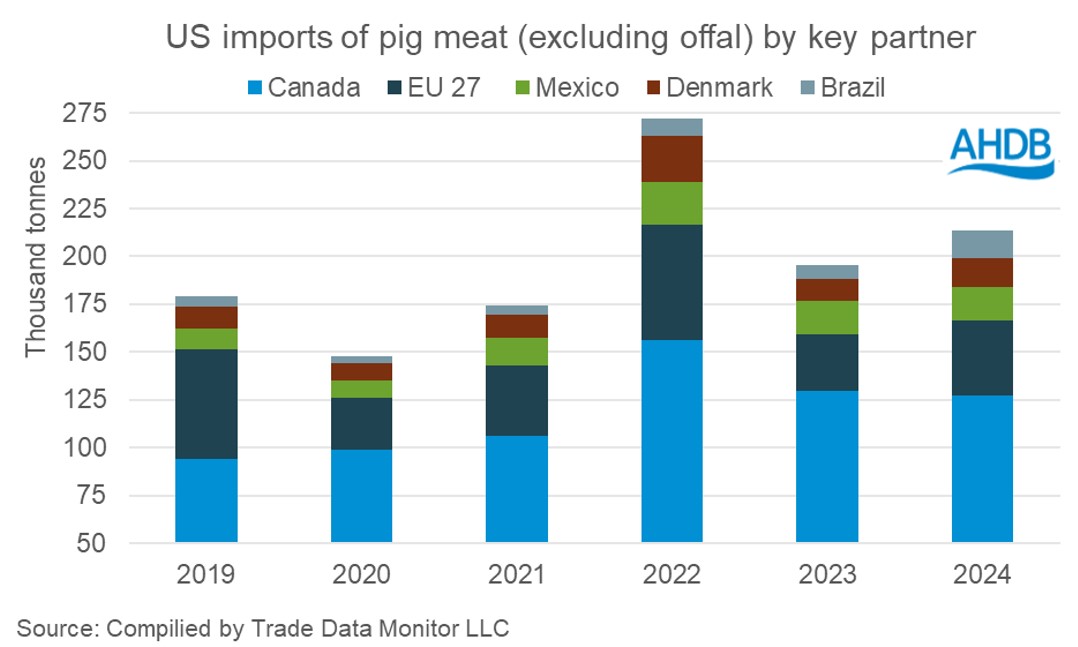

The US remains a key importer of pig meat on the global market. So far this year (Jan-May) imports (excluding offal) totalled 202,200 tonnes, a 7.5% increase year on year. Good demand in the domestic market, supported by higher prices for competing proteins, is reported as a key driver.

Canada remains the most significant provider of pork to the US holding a 63% market share. However, imports from Canada have declined 1.6% to 127,500t. Imports from the EU27 are up by over 9,000 tonnes year on year, now taking a 19% market share of US import volume. UK shipments to the US totalled 2,400 tonnes Jan-May.

{kind=link}